The rising cost of personal insurance can be frustrating, especially if you've maintained a clean driving record and haven't filed a claim. But know that insurance premiums aren't rising on a whim. Consumers across the U.S. have been dealing with a challenging insurance landscape for several years now. It's known as a "hard market" in insurance parlance, and no one knows when it might end.

Several factors are responsible:

1. Climate Change and Natural Disasters: As climate change intensifies, the frequency and severity of weather-related natural disasters has increased. This has resulted in higher claim payouts by insurance companies, driving up home insurance premiums.

2. Advances in Technology: While technology has improved vehicle safety, it has also made repairs more expensive. Newer models are laden with expensive sensors and electronic systems, which increase repair costs after an accident, thereby raising auto insurance premiums.

3. Rising Medical Costs: With health care costs on the upswing, the medical expenses associated with auto accidents are increasing. This has contributed to higher auto insurance premiums as insurers need to cover these ballooning costs.

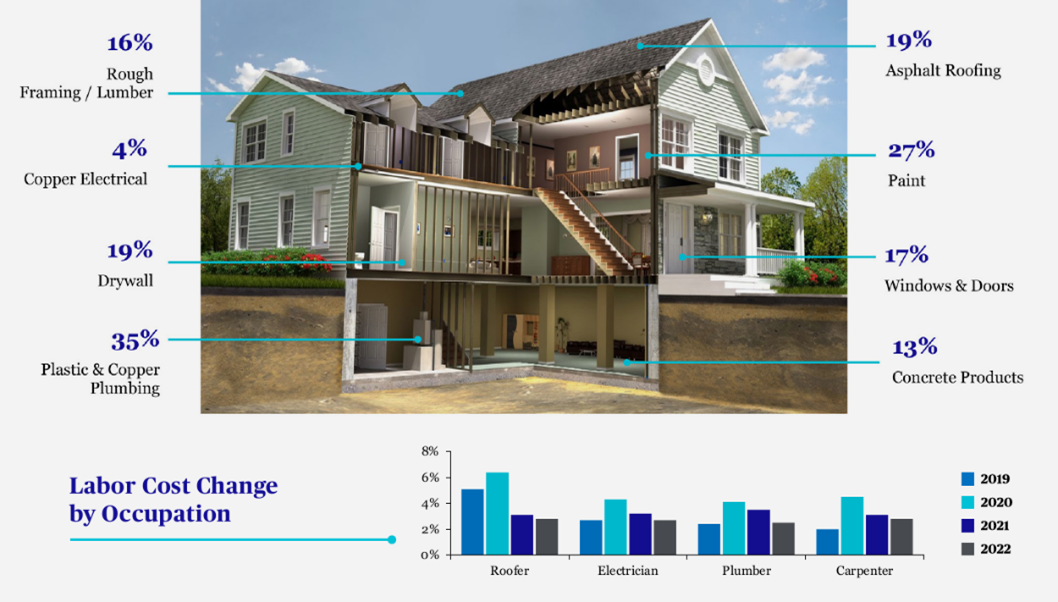

4. Home Renovations and Increased Value of Home Goods: As homeowners make improvements to their homes and the cost of building materials and home goods increases (see chart below), the potential payout an insurer might face in the event of a claim also rises. Consequently, home insurance premiums increase to cover these potential costs.

Ways to reduce your premiums

It may feel otherwise, but you're not at the mercy of the insurance companies. Here are several steps policyholders can take to keep their insurance premiums under control:

1. Bundle Insurance Policies: Many insurance companies offer discounts for "bundling," or buying more than one type of policy from the same company. Consider getting both your auto and home insurance from the same insurer to lower your premiums.

2. Perform Preventative Maintenance. Regular maintenance ensures your vehicle is safe to drive, which could help you avoid accidents and the subsequent claims that could increase your premium. For home insurance, preventative maintenance might include regularly checking and repairing roofing, plumbing, electrical systems, and heating, ventilation, and air conditioning (HVAC) units. These checks can prevent issues such as water leaks, fires, or other damage that could lead to insurance claims. Like with auto insurance, fewer claims typically result in lower premiums.

2. Increase Your Deductible: A higher deductible — the amount you have to pay out of pocket for a claim before your insurance kicks in — can lower your premiums. But remember, if you need to make a claim, you'll be responsible for that deductible.

3. Take Advantage of Discounts: Many insurers offer discounts for safety features, like security systems and water-leak detectors in homes or safety equipment in cars. Additionally, maintaining a good driving record or a claims-free history on your home can lead to discounts on your premiums.

4. Regularly Review and Update Your Policy: Your insurance needs may change over time, and it's possible you're paying for more coverage than you need. Regularly reviewing your policy and making necessary adjustments can help keep premiums under control.

Rising home and auto insurance premiums may be inevitable, given the various influencing factors. But armed with the right information and tactics, consumers can play an active role in managing these costs. By being proactive, it is entirely possible to balance necessary coverage with affordable premiums.

Get in Touch With Our Team Today

Proud partner of Assurex Global

$45B+

TOTAL PREMIUM MANAGED ANNUALLY

730+

PARTNER OFFICES

25,000+

EMPLOYEES